Default Investment Strategy (“DIS”) is a ready-made investment arrangement mainly designed for those members who are not interested or do not wish to make a fund choice, and is also available as an investment choice itself, for members who find it suitable for their own circumstances. For those members who do not make an investment choice, their future contributions and accrued benefits transferred from another MPF scheme (collectively, “Future Investments”) will be invested in accordance with the DIS. The DIS is required by law to be offered in every MPF scheme and is designed to be substantially similar in all MPF schemes.

Objective and Strategy

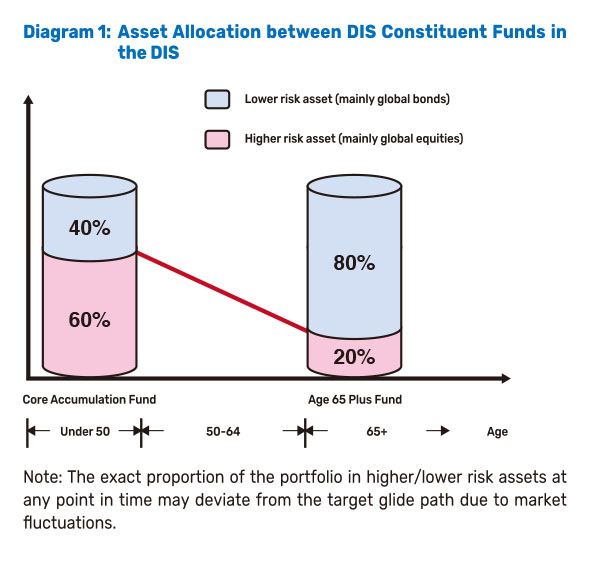

The DIS aims to balance the long term effects of risk and return through investing in two constituent funds, namely the Core Accumulation Fund (“CAF”) and the Age 65 Plus Fund (“A65F”), according to the pre-set allocation percentages at different ages. The CAF will invest around 60% in higher risk assets (higher risk assets generally mean equities or similar investments) and 40% in lower risk assets (lower risk assets generally mean bonds or similar investments) of its net asset value whereas the A65F will invest around 20% in higher risk assets and 80% in lower risk assets. The DIS Constituent Funds adopt globally diversified investment principles and use different classes of assets, including global equities, fixed income, money market and cash, and other types of assets allowed under the MPF legislation.

Annual de-risking

Accrued benefits invested through the DIS will be invested in a way that adjusts risk depending on a member’s age. The DIS will manage investment risk exposure by automatically reducing the exposure to higher risk assets and correspondingly increasing the exposure to lower risk assets as the member gets older. Such de-risking is to be achieved by way of reducing the holding in the CAF and increasing the holding in the A65F over time. Diagram 1 above shows the target proportion of investment in riskier assets over time. The asset allocation stays the same up until 50 years of age, then reduces steadily until age 64, after which it stays steady again.

In summary, under the DIS:

1) When a member is below the age of 50, all accrued benefits and Future Investments will be invested in the CAF.

2) When a member is between the ages of 50 and 64, all accrued benefits and Future Investments will be invested according to the allocation percentages between the CAF and A65F as shown in the DIS de-risking table (as per Diagram 2 below). The de-risking on the existing accrued benefits and Future Investments will be automatically carried out as described above.

3) When a member reaches the age of 64, all accrued benefits and Future Investments will be invested in the A65F.

Diagram 2: DIS De-risking Table

|

Age |

Core Accumulation Fund(“CAF”) |

Age 65 Plus Fund(“A65F”) |

|

Below 50 |

100.0% |

0.0% |

|

50 |

93.3% |

6.7% |

|

51 |

86.7% |

13.3% |

|

52 |

80.0% |

20.0% |

|

53 |

73.3% |

26.7% |

|

54 |

66.7% |

33.3% |

|

55 |

60.0% |

40.0% |

|

56 |

53.3% |

46.7% |

|

57 |

46.7% |

53.3% |

|

58 |

40.0% |

60.0% |

|

59 |

33.3% |

66.7% |

|

60 |

26.7% |

73.3% |

|

61 |

20.0% |

80.0% |

|

62 |

13.3% |

86.7% |

|

63 |

6.7% |

93.3% |

|

64 and above |

0.0% |

100.0% |

Note: The above allocation between CAF and A65F is made at the point of annual de-risking and the proportion of the CAF and the A65F in the DIS portfolio may vary during the year due to market fluctuations.

More

Fees and out-of-pocket expenses of the CAF and A65F

The aggregate of the payments for services of the CAF and the A65F must not, in a single day, exceed a daily rate of 0.75% per annum of the net asset value (“NAV”) of each of the DIS Constituent Funds divided by the number of days in the year. It includes, but is not limited to, the fees paid or payable for the services provided by the trustee, the administrator, the investment manager(s), the custodian and the sponsor and/or the promoter of the Scheme and the underlying investment fund(s) of the respective DIS Constituent Funds, and any of the delegates from these parties and such fees are calculated as a percentage of the NAV of each of the DIS Constituent Funds and its underlying investment fund(s), but does not include any out-of-pocket expenses incurred by each DIS Constituent Fund and its underlying investment fund(s).

The total amount of all payments that are charged to or imposed on the DIS Constituent Funds or members who invest in DIS Constituent Funds, for out-of-pocket expenses incurred by the trustee on a recurrent basis in the discharge of the trustee’s duties to provide services in relation to the DIS Constituent Funds, shall not in a single year exceed 0.2% of the NAV of each of the DIS Constituent Funds. For this purpose, out-of-pocket expenses include, for example, annual audit expenses, printing or postage expenses relating to recurrent activities (such as issuing annual benefit statements), recurrent legal and professional expenses, safe custody charges which are customarily not calculated as a percentage of NAV and transaction costs incurred by a DIS Constituent Fund in connection with recurrent acquisition of investments for the DIS Constituent Fund (including, for example, costs incurred in acquiring underlying investment funds) and annual statutory expenses (such as compensation fund levy where relevant) of the DIS Constituent Fund.

Out-of-pocket Expenses that are not incurred on a recurrent basis may still be charged to or imposed on the DIS Constituent Funds, and do not subject to the statutory limit.

How does DIS affect you?

If you have accounts in the Scheme that are set up before the April 1, 2017 (“pre-existing accounts”), depending on whether you have previously made any fund choices, it may affect you in different ways:

1) If you have already given a valid specific investment instruction for the accrued benefits and Future Investments in your pre-existing account or you are 60 years old or above before the April 1, 2017, you will not be affected by the implementation of the DIS.

2) If all your accrued benefits in a pre-existing account are invested in the existing default arrangement (“Existing Default Arrangement”, i.e. investing in all constituent funds in equal shares) as at April 1, 2017 and you have not given a valid specific investment instruction for the pre-existing account, you will receive a separate notice (i.e. the “DIS Re-Investment Notice”) sent to you on or before the end of September 2017. The DIS Re-Investment Notice will explain that if you do not make an investment choice by replying within a specified timeline, your accrued benefits in the Existing Default Arrangement will be redeemed in whole and re-invested in accordance with the DIS. Therefore, if you receive the DIS Re-Investment Notice, please pay special attention to the contents and make appropriate arrangement. You should note that Existing Default Arrangement include the investment in the Guaranteed Fund which provides guarantee, but the default investment strategy does not provide such guarantee and the risk of the Existing Default Arrangement (the risk levels are ranged from “low” to “high”) may be different from that of the DIS (the risk level are ranged from “low to medium” to “medium to high”) and you may be exposed to market risks as a result of any reinvestment of your accrued benefits in the DIS.

There are special circumstances.

- Where the accrued benefits in pre-existing account transferred from another account within the Scheme (e.g. in the case of cessation of employment, where accrued benefits in your contribution account are transferred to a personal account within the Scheme), your accrued benefits in the pre-existing account will be invested in the same manner as they were invested immediately before the transfer but your future contributions or accrued benefits transferred from another scheme may be invested in the DIS after the implementation of the DIS, unless otherwise instructed.

- For the accrued benefits of your pre-existing account which are only invested according to the Existing Default Arrangement, parts of those accrued benefits have been invested in the Guaranteed Fund. Where a guarantee value of those accrued benefits investing the Guaranteed Fund of yours greater than its market value to be paid to the member upon the expiry of the 42-days period from the date of issuance of DRN or the expiry of the 60-day period for un-located members, the above rules will not apply for the member (i.e. those accrued benefits investing the Guaranteed Fund will remain unchanged). For the future contributions and/or accrued benefits transferred from another scheme for that member on or after the expiry of the 42-days period from the date of issuance of DRN or the expiry of the 60-day period for un-located members , these contributions and/or accrued benefits transferred from another scheme will be invested into the DIS. You could obtain the valuation result of the accrued benefits investing in the Guaranteed Fund by calling our hotline at 2533 5522 on or after the expiry of the 42-days period from the date of issuance of DRN or the expiry of the 60-day period for un-located members. The valuation result would also be shown in the confirmation statement issued to you not later than 5 business days after the dealing day on which (i) all relevant accrued benefits in pre-existing account are invested into the DIS or (ii) the Accrued Benefits (other than the Accrued Benefits in the Guaranteed Fund) in Pre-existing Account are invested into the DIS.

3) If part of your accrued benefits in a pre-existing account is invested in the Existing Default Arrangement, unless the Trustee has received any specific investment instructions, your accrued benefits will be invested in the same manner as accrued benefits were invested immediately before the April 1, 2017. Future Investments will be invested in accordance with DIS.

Distribution schedule of DIS-related notice

DIS Pre-Implementation Notice (“DPN”)

Inform the member about the important changes to the Mandatory Provident Fund Schemes Ordinance will take effect on April 1, 2017. From April 1, 2017, the default investment arrangement of the Scheme will be the DIS replacing the existing default fund of the Scheme.

DIS Re-Investment Notice (“DRN”)

If all the accrued benefits in a pre-existing account are invested in the existing default arrangement (“Existing Default Arrangement”, i.e. investing in all constituent funds in equal shares) as at April 1, 2017 and the member have not given a valid specific investment instruction for the pre-existing account, the member will receive DRN on or before the end of September 2017. The DRN will explain that if a member does not make an investment choice by returning the completed “Option 2 Form” to us within a specified timeline, member’s accrued benefits investing in the Existing Default Arrangement will be redeemed in whole and re-invested in accordance with the DIS. Therefore, if you receive the DRN, please pay special attention to the contents and make appropriate arrangement.